The International Monetary Fund’s (IMF) recent description of Qatar as a “model of resilience” reflects something that is increasingly visible on the ground, but not always fully understood. The label itself is not new. What is changing is what sits behind it. The resilience Qatar is demonstrating today is fundamentally different from what defined it ten or even five years ago.

For a long time, resilience here was essentially shorthand for hydrocarbon strength. Liquefied natural gas (LNG) insulated the economy, underpinned fiscal stability, and provided a reliable buffer against external shocks. That remains true. But it is no longer the full story, and it is certainly not the defining one.

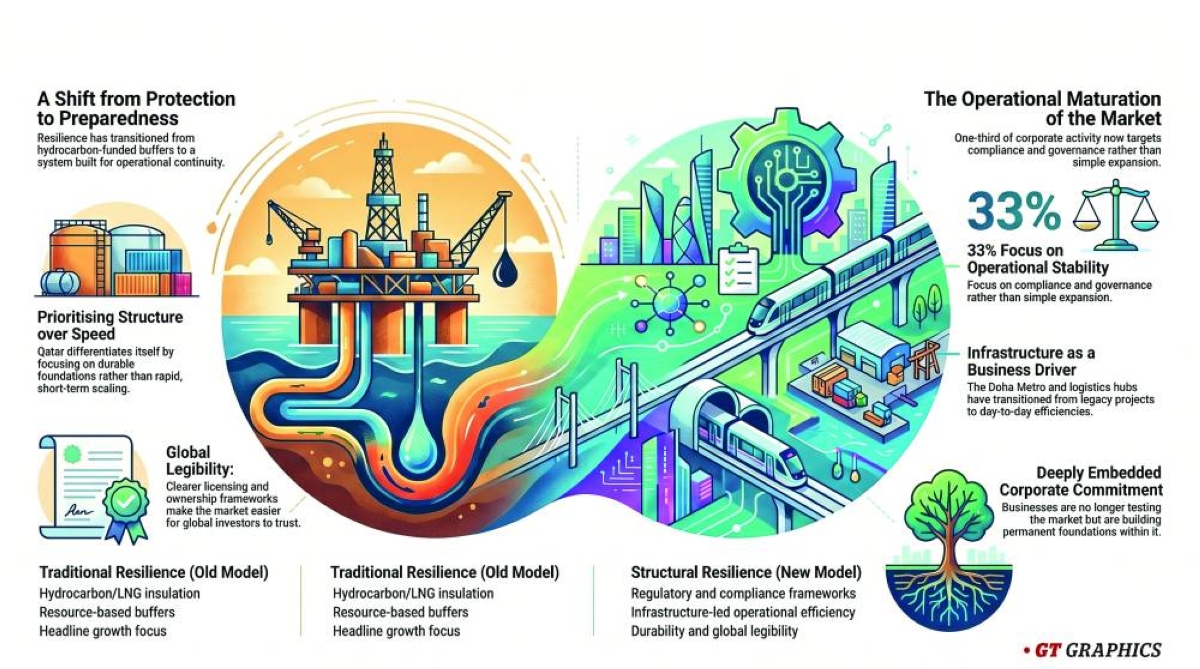

What is emerging now is a different kind of resilience, built less on resources and more on structure.

Spend time with businesses operating in Qatar and a clear pattern emerges. The conversation is no longer about entering the market, but about how deeply companies are embedded within it. That is borne out in day-to-day conversations with business owners, leaders and investors, where the focus has shifted towards licence stability, compliance frameworks, workforce continuity, and internal governance. At Sovereign PPG, roughly a third of all our corporate activity now sits in these operational and regulatory areas rather than expansion.

That tells you something important. That companies are not testing the market, they are committed to building around it. And in a more uncertain global environment, that behaviour says more about economic durability than headline growth ever will.

This is where the IMF’s assessment starts to carry real weight. It reflects an economy that is being shaped from within, not just measured from above.

That shift is often described as diversification, but the term is used too loosely. The focus tends to be on sectors such as finance, tourism, and logistics – and yes, those are expanding. The Qatar Financial Centre (QFC) is playing a growing role in attracting international firms. Tourism has moved beyond the one-off surge of the World Cup into something more sustained. And logistics infrastructure – from Hamad Port to Hamad International Airport – is steadily reinforcing Qatar’s position as a regional connector.

But diversification is not really about what grows. It is about how it is built. This is where Qatar is beginning to stand out. In a Gulf context often associated with speed – rapid scaling, fast capital, quick wins – it is taking a different path, prioritising structure over speed.

That may sound less exciting, but it is far more durable. And increasingly, it is becoming a key competitive advantage.

The regulatory environment is central to that. Clearer licensing pathways, foreign ownership frameworks, and internationally aligned platforms like the QFC have reduced the friction that typically comes with entering emerging markets. More importantly, they make companies easier for global investors to understand and trust.

That reduces many of the structural concerns that tend to shape “emerging market” perceptions in the first place. For investors, predictability matters as much as opportunity – and Qatar is offering both.

The result is a business environment that is easier to assess, easier to understand, and ultimately easier to invest in. Companies are structured to be globally legible from the outset, rather than treated as exceptions.

This has practical consequences. Capital moves with greater confidence, due diligence becomes more straightforward, and businesses can scale without repeatedly reworking their foundations. Over time, that shifts the balance of the economy towards a more capable and confident private sector that plays a greater role in driving growth.

This is where infrastructure comes back into the picture, though not in the way it is often discussed.

Much of Qatar’s pre-World Cup investment cycle was once criticised as excessive or overly ambitious. But that framing misses what is becoming clear on the ground – that they legacy is not sitting idle, it is actively shaping how the economy functions.

Take the Doha Metro. It is not just a visible marker of development, it is changing day-to-day business conditions in ways that are easy to overlook but hard to ignore once you are in the market. Commutes are shorter, cross-city access is easier, and the day-to-day challenges of doing business across the city has been reduced.

For companies operating here, those are not abstract efficiencies. They show up in staffing decisions, logistics planning, and how quickly teams can scale across locations. And over time, they compound.

That is why Qatar’s resilience looks different today. It is no longer simply about absorbing shocks. It is about whether the underlying system allows businesses to keep operating smoothly when conditions shift. Seen from that perspective, the shift is less about protection and more about preparedness.

None of this diminishes the role of hydrocarbons. LNG will remain central to Qatar’s economy for years to come. But its role is changing. It is no longer the only pillar holding the system up, it is one of several.

As the private sector deepens and the economy becomes more structurally mature, dependence on hydrocarbons becomes less defining of the whole system.

There are still gaps to close. Diversification needs greater scale. Regional competition is intensifying. And building the human capital required for a more complex economy will take time. But Qatar’s trajectory is deliberate, and more coherent than it is often given credit for.

The IMF has recognised Qatar’s resilience. But the more useful lens is not the label itself, but what sits behind it. This is no longer an economy defined primarily by what it produces, but by how it is organised.

And what is increasingly evident on the ground is that Qatar is not redefining its foundations. It is reinforcing the structure built around them.

- Neil Wilson is the MD of Sovereign PPG Qatar, part of the Sovereign Group, a leading corporate service provider across the GCC.